Australia has gone through many things throughout the last century, from its involvement in 10 wars as well as massive bush fire seasons year after year. All these detrimental factors, yet three Australian cities still made it into the top 10 most liveable cities in the world index. However, little does everyone know that Australia is approaching another crisis, maybe not on an international scale like the others, but large enough to be considered a crisis. The crisis being, the inflation of the ‘real estate’ or housing market in Australia.

Over the last few decades the house prices in Australia have increased exponentially especially in the two largest cities also being some of the most liveable in the world. The constant increase of house prices over the past few decades in economical terms is known as inflation. The table below The term ‘housing affordability‘ is used to describe the relation between the expenditure of monetary resources one would spend on housing (prices, rents and mortgages), and the household income. Both high inflation in the market and housing affordability being low contribute to cause a number of problems for Australians.

| March 1980 | March 2016 | |

|---|---|---|

| Sydney* | $64 800 | $999 600 |

| Melbourne | $40 800 | $713 000 |

| Brisbane* | $34 500 | $480 000 |

| Adelaide | $36 300 | $445 000 |

| Perth | $41 500 | $520 000 |

| Canberra | $39 700 | $570 000 |

| Hobart | Not available | $385 000 |

| Darwin | Not available | $582 500 |

People effected because of the inflation in prices would be the younger generation of Australians who would not be able to afford to move out of their parents house. Significantly diminishing chances for these individuals, the future of Australia to even live the “Australian Dream.” 63% of Australians believe that it is impossible for the younger generation to own a house in the future. Overall causing more young people to live with their parents and discouraging entrance into the market.

So how much does it actually cost to own a house? Take the example of Melbourne, with the median weekly wage (after tax) of an individual living in Melbourne being $778.96. Crazily, the estimated weekly repayment inclusive of interest and principal is $778 for an average house. Meaning an astonishing amount of ones weekly wage, exactly 99.88% goes towards ones house. But this is for one with a median wage, imagine how hard it would be owning a house as a single parent, or working on minimum wage and supporting family.

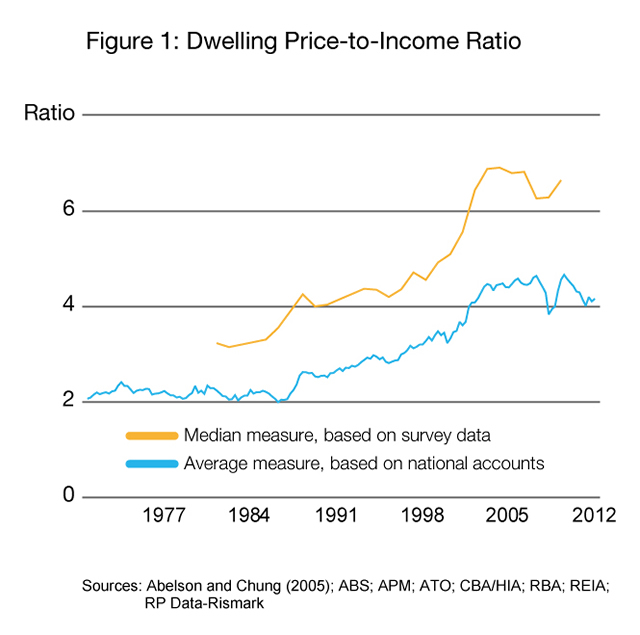

The decline of the affordability factor since the 1980s is shown in the OECD’s price to income index which is depicts nationwide average house price increase of 78% from may 1980. With the ageing population of Australia, the fact that majority of the homes occupied in the more prominent suburbs of Melbourne are occupied by older families is not a surprise too many, but what does this do to the economy. This makes new home buyers and people who want to move into these prominent suburbs pay more money for a home in that particular suburb to encourage people to sell, which would be one of the primary causes of inflation.

1.7 Trillion Australian Dollars is held by the banks in mortgages for owner/occupiers and investors, which is the highest in any western country in the world. Meaning that if the economy collapsed, and people were to lose their jobs, many people would not be able to afford to pay off their mortgages and eventually people would lose their homes.

Ultimately, although there were many different causes contributing to the massive increase of pricing, the numerous list of causes has a more numerous list of outcomes due to the constant increase of prices and decrease of affordability. Overall I believe, the housing economy of Melbourne is overly inflated and very susceptible to ‘bursting’ and causing more problems for Australians. The unaffordability of housing, and inflation of prices will be the downfall of the economy, affecting all Australians, and ultimately be the downfall of us all.

References

- https://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Library/pubs/BriefingBook45p/HousingAffordability

- https://www.abc.net.au/news/2019-10-11/housing-affordability-younger-australians-buying-australia-talks/11549210

- https://mhseco19.home.blog/2019/03/01/rising-living-cost-and-inflation/

- https://www.openagent.com.au/blog/salary-needed-to-afford-a-house-in-australia

- https://grattan.edu.au/wp-content/uploads/2018/03/901-Housing-affordability.pdf

Great use of graphs – hopefully you’ve learnt enough to counter older Australian’s arguments when they just say that young people need to save more and stop going out for brunch! Did you see this – https://www.theguardian.com/lifeandstyle/2017/may/15/australian-millionaire-millennials-avocado-toast-house

LikeLike

This was very interesting. As this issue is very relevant to our generation today, I found this article very eye-opening to the fact that people are finding it harder and harder to afford houses and that when our time comes around to buy houses it will be even harder.

LikeLike

So good! Loved how succinct it was.

LikeLike

Very good analysis, loved the use of graphs on an issue most relevant to us young people.

LikeLike

Very in depth and informative. Good use of links and clearly done your research. Great Job A.K.

LikeLike